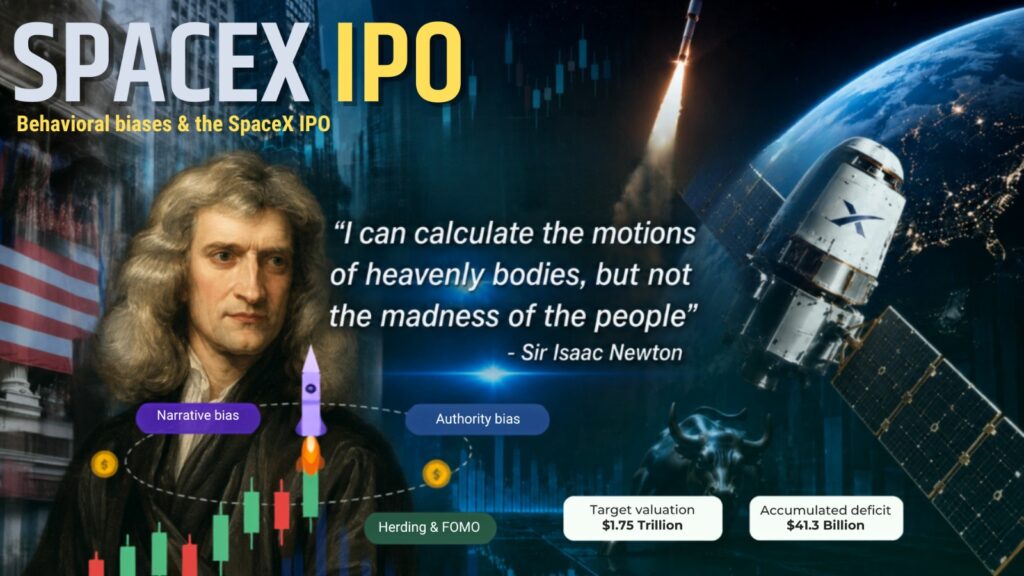

Isaac Newton, widely regarded as one of history’s greatest analytical minds, reportedly lost a fortune in the South Sea Company bubble of 1720. He is said to have reflected, with characteristic precision, that he could “calculate the motions of heavenly bodies, but not the madness of the people.” Three centuries later, as Elon Musk prepares to take SpaceX public in what is being positioned as the largest IPO in history — targeting a $1.75 trillion valuation and a $75 billion raise on the Nasdaq — Newton’s lament feels eerily relevant.

The SpaceX IPO is not merely a financial event. It is a behavioral experiment — one being conducted at planetary scale.

The Anatomy of the Offering

The numbers deserve to be stated plainly. SpaceX filed its S-1 prospectus with the U.S. Securities and Exchange Commission in May 2026, revealing, for the first time, the audited financial reality of Elon Musk’s rocket empire. In 2025, the company posted a net loss of $4.9 billion on revenue of $18.7 billion. In Q1 2026 alone, the loss widened to $4.3 billion on $4.7 billion in revenue. The company carries an accumulated deficit of $41.3 billion since inception.

Starlink, the satellite internet division, is the genuine business engine — profitable, growing, and responsible for nearly 70% of revenues. Starlink recorded an operating profit of $4.4 billion in 2025 and has surpassed 10.3 million subscribers across 164 countries. But the AI segment — born of SpaceX’s all-stock acquisition of Musk’s own company xAI in February 2026 — recorded an operating loss of $6.35 billion in 2025 alone. In Q1 2026, xAI burned $2.47 billion while generating only $818 million in revenue.

Wall Street is being asked to underwrite a 20% compound annual growth rate sustaining revenue expansion of roughly 38-fold by 2046. That is not a forecast. That is science fiction with a term sheet.

Bias #1: Narrative Bias — When a Story Replaces a Spreadsheet

Behavioral finance research consistently documents the power of narrative in investor decision-making. Kahneman and Tversky’s System 1 thinking tells us that the human brain is evolutionarily primed to respond to stories, not statistics. SpaceX’s prospectus is, at 200,000 words, the most extraordinary document ever filed with the SEC — part Asimov, part Heinlein, part business plan. Its stated mission: to *”extend the light of consciousness to the stars.”*

That language is not incidental. It is engineered to bypass rational valuation and appeal directly to the limbic system. Investors who imagine themselves as co-owners of humanity’s multiplanetary future are far less likely to question why a company burning $4.3 billion in a single quarter is being priced at $1.75 trillion.

Practically speaking, the antidote to narrative bias is forensic decomposition. A disciplined investor must separate the emotional storyline from the economic substance. Ask: Which specific segment generates actual profits today? What is the path to profitability for the loss-making segments? Starlink’s ARPU has, in fact, fallen from $99/month in 2023 to $66 in Q1 2026, even as subscriber numbers grow — a compression that raises long-term margin questions that the narrative of cosmic ambition conveniently obscures.

Bias #2: Authority Bias — Musk as a Cognitive Shortcut

Authority bias describes our tendency to defer to perceived experts or high-status individuals, using their confidence as a substitute for our own analysis. Elon Musk is, arguably, the most powerful single vector of authority bias in modern financial markets. His track record — Tesla, Falcon 9’s reusability, Starlink’s execution — provides a powerful heuristic: if Musk is building it, it works

But authority bias is particularly dangerous when the authority in question holds structural control that removes accountability. The SpaceX prospectus discloses that Musk retains 85.1% of combined voting power through a dual-class stock structure. He cannot be removed without his own consent. As the Times of India noted in a recent editorial commentary, conflicts of interest are not incidental to the structure — they are the structure.

History is instructive here. Authority bias drove retail participation in Masayoshi Son’s SoftBank Vision Fund investments, in Adam Neumann’s WeWork, and in countless promoter-led IPOs in Indian markets. The persona of the founder became a substitute for fundamental analysis, with predictable results.

The practical corrective: evaluate the asset, not the celebrity. Would you invest in a company with a $41 billion accumulated deficit and a widening quarterly loss at a $1.75 trillion valuation if the founder were unknown? That question, applied rigorously, is the behavioral inoculation against authority bias.

Bias #3: Herding and FOMO — The Index Trap

Perhaps the most structurally insidious dimension of the SpaceX IPO is the deliberate engineering of what behavioral economists call herding — the tendency of investors to follow the crowd rather than conduct independent analysis. SpaceX’s listing was timed to exploit Nasdaq’s “fast entry” rule, under which a sufficiently large company joins the Nasdaq-100 after only 15 trading days, compared to the customary year. FTSE Russell shortened its window further, to five days.

The consequence is mechanical. Any investor holding a Nasdaq-100 ETF or Russell index fund will own a piece of SpaceX whether they have chosen to or not. This creates what market observers call “forced buying” — institutional herding at scale. The retail investor sees SPCX appear in their index portfolio and interprets its presence as validation. After all, if the index holds it, it must be sound.

This is the FOMO feedback loop made structural: the listing triggers index inclusion, which triggers buying, which drives up the price, which reinforces the narrative that the market knows something you don’t. In my book *The Behavioral Finance Way — A Practical Guide to Mindful Investing*, I describe this as the difference between investing with conviction and investing with crowd. The crowd, in this case, includes the algorithmic machinery of global ETFs.

The corrective for individual investors: Passive index exposure is a legitimate investment approach, but it is not a substitute for conscious portfolio construction. If an investor’s index exposure already creates SpaceX participation, there is no rational case for adding a discretionary IPO allocation unless the fundamental analysis independently supports it.

How Should a Normal Investor Evaluate This Opportunity?

Three steps, applied sequentially, can convert behavioral impulse into rational decision-making:

Step 1 — Decompose the business. Starlink is a real, profitable business. The Space launch segment is viable but capital-intensive. The AI/xAI segment is, at present, a high-burn, early-stage venture inside a public company. Price accordingly. Do not pay a $1.75 trillion enterprise value for the combined entity as if all three segments carry Starlink’s quality of earnings.

Step 2 — Assess governance risk explicitly. With 85.1% voting control vested in a single individual, investors are purchasing an economic exposure they cannot influence. This is not necessarily disqualifying — Berkshire Hathaway’s structure concentrates authority similarly — but it demands a conscious premium for governance risk, not the discount that emotional enthusiasm typically applies.

Step 3 — Size the position to the actual conviction. If, after completing steps one and two, the investment still merits inclusion, allocate proportionately to its risk profile in the overall portfolio — not to the size of the hype. A 2% satellite-internet/space infrastructure allocation in a diversified portfolio is a coherent investment thesis. Liquidating fixed income to chase the listing day is a behavioral event, not an investment decision.

A Closing Note

The South Sea Company promised exclusive access to the riches of South America. SpaceX promises the entire solar system. The ambition is grander; the pattern is familiar. Financial gravity, as one commentator has observed, no longer appears to apply — right up until it does.

For investors, the most valuable tool in evaluating the SpaceX IPO is not a discounted cash flow model, though that helps. It is self-awareness — the recognition of which parts of your enthusiasm are data-driven and which parts are the product of a story told extraordinarily well.

As I often remind clients: the market will always offer another opportunity. The behavioral biases that compromise our judgment in moments of extraordinary hype are the real permanent risks to long-term wealth creation. Discipline isn’t the absence of ambition. It is the structure that makes ambition sustainable.

Disclaimer: This article is for educational and informational purposes only and does not constitute investment advice or a recommendation to buy, sell, or hold any security. The views expressed are based on the author’s research and expertise in behavioral finance and wealth management. Prof. Dr. Meghna Dangi is not a SEBI-registered investment advisor. This is not a promotional endorsement of any specific financial product or institution.