The Paradox of Investing

For decades, investors have searched for the perfect formula to build wealth. Some chase the best-performing mutual funds, others attempt to predict market movements, while many wait endlessly for the “right time” to invest. Yet one of the most comprehensive studies on Systematic Investment Plans (SIPs) suggests that successful investing may be far simpler than most people believe.

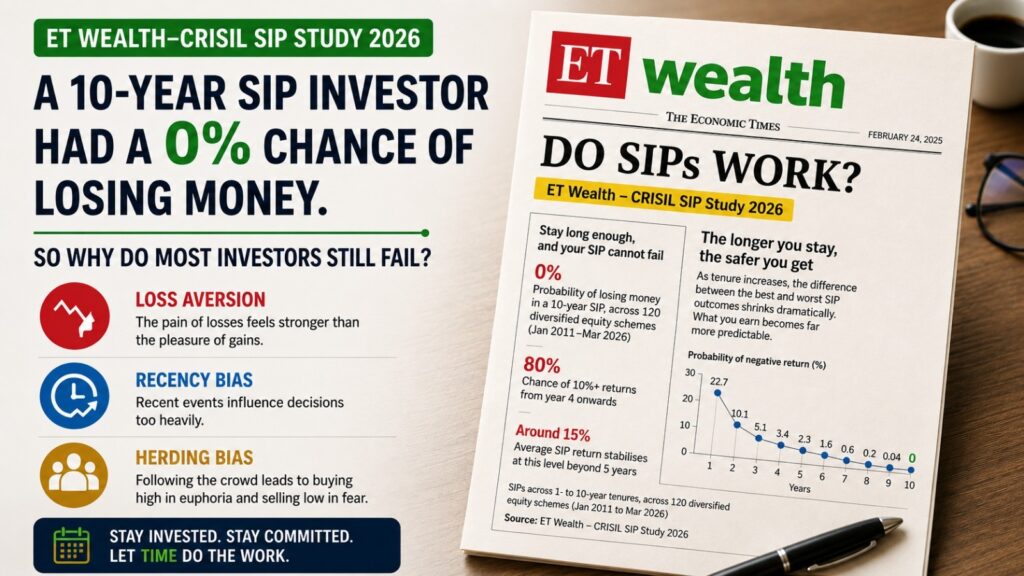

The latest ET Wealth–CRISIL SIP Study 2026 analysed 120 diversified equity mutual fund schemes over the period January 2011 to March 2026. Its findings were striking. A 10-year SIP investor had virtually a 0% probability of losing money. The probability of loss declined from 23% in a one-year SIP to zero over a ten-year period. Even the worst observed 10-year SIP outcome generated approximately 7% annualised returns, while average returns stabilised around 15% beyond five years. More importantly, from the fourth year onwards, investors enjoyed an 80% probability of earning annualised returns exceeding 10%.

These findings reinforce a principle that financial theory has advocated for years: time has a remarkable ability to reduce the impact of market volatility. Yet an uncomfortable question remains. If long-term SIP investing is statistically so effective, why do many investors fail to achieve these outcomes? The answer lies not in markets, mutual funds, economic forecasts, or fund managers. It lies in human behaviour.

The Gap Between Investment Returns and Investor Returns

One of the most overlooked realities in investing is that investment returns and investor returns are often very different. A mutual fund may deliver exceptional long-term performance, yet many investors fail to capture those returns because of the decisions they make along the way. Research across global markets has consistently shown that investors tend to invest more after markets have risen substantially and withdraw money after markets have fallen. In effect, they buy high and sell low. While this behaviour may appear irrational when viewed retrospectively, it is remarkably common. Investors often respond to emotions rather than evidence, allowing fear and optimism to influence decisions that should ideally be driven by long-term objectives. As a result, the biggest threat to wealth creation is often not selecting the wrong investment product. It is abandoning the right investment strategy at the wrong time.

Why Falling Markets Feel More Painful Than Rising Markets Feel Rewarding

Market declines affect investors not only financially but emotionally. Human beings naturally experience the pain of losses more intensely than the satisfaction derived from equivalent gains. A portfolio decline of 15% therefore feels significantly more impactful than the pleasure generated by a subsequent 15% gain. This emotional asymmetry can distort decision-making. Temporary market corrections begin to feel permanent, and investors start questioning strategies that were originally designed for long-term horizons. Ironically, SIPs are specifically structured to benefit from falling markets. Lower prices allow investors to accumulate more units with the same investment amount. When markets eventually recover, these additional units contribute meaningfully to long-term returns. However, because investors focus on short-term losses rather than long-term opportunities, many discontinue their SIPs precisely when they are positioned to generate the greatest future benefit.

The Dangerous Influence of Recent Events

Human beings naturally give disproportionate importance to recent experiences. In investing, this tendency can be particularly costly. When markets rise continuously, investors begin to believe that positive returns will persist indefinitely. Conversely, during market downturns, pessimism dominates expectations and investors assume that further declines are inevitable. Recent events begin to overshadow decades of historical evidence. The ET Wealth–CRISIL study provides an important counterpoint to this tendency. As the investment horizon increased, the gap between the best and worst SIP outcomes narrowed considerably. Returns became increasingly predictable, while the probability of loss steadily declined. What appears alarming in the short term often becomes insignificant over a sufficiently long investment horizon. The lesson is clear: market noise is temporary, but disciplined investing benefits from permanence.

The Cost of Following the Crowd

Financial markets are inherently social environments. Investors are constantly exposed to opinions from television experts, social media influencers, colleagues, relatives, and friends. While access to information has increased dramatically, so has the temptation to follow the crowd. During bull markets, investors often feel compelled to participate aggressively because everyone around them appears to be making money. During market corrections, the same investors feel pressured to exit because fear becomes the dominant narrative. History repeatedly demonstrates that collective sentiment is often least reliable at extremes. Excessive optimism frequently appears near market peaks, while excessive pessimism often emerges near market bottoms. Investors who allow public sentiment to dictate their decisions may find themselves consistently reacting rather than investing. Long-term wealth creation requires conviction, and conviction is often tested most when popular opinion suggests doing the opposite.

SIPs Are a Commitment Device, Not Just an Investment Tool

Most discussions around SIPs focus on concepts such as rupee-cost averaging and the power of compounding. While both are important, they do not fully explain why SIPs are such effective wealth-building tools. A SIP is also a commitment device. By automating the investment process, it reduces the need for repeated decision-making and limits the temptation to time the market. Investors no longer need to decide whether today is a good day to invest; the process continues irrespective of market sentiment. This seemingly simple feature creates a powerful advantage. Automation removes emotion from the equation and replaces it with consistency. In many ways, the true strength of a SIP lies not in its mathematics but in its ability to protect investors from their own impulses.

The Real Measure of Investment Success

The findings of the ET Wealth–CRISIL SIP Study provide compelling evidence that long-term disciplined investing works. However, they also highlight an uncomfortable truth. The challenge for most investors is not finding an appropriate investment strategy; it is remaining committed to that strategy through periods of uncertainty. Market corrections, geopolitical tensions, economic slowdowns, inflation concerns, and alarming headlines will always exist. Every generation of investors encounters reasons to doubt the future. Yet wealth has historically been created not by those who successfully predicted every market movement, but by those who remained invested despite uncertainty. The investors who ultimately benefit from compounding are not necessarily the smartest, wealthiest, or most informed. More often, they are the individuals who display patience when patience is difficult and discipline when discipline is uncomfortable.

Conclusion: The Greatest Risk Is Often Ourselves

The finding that a 10-year SIP investor had virtually no chance of losing money should be viewed as more than just an endorsement of systematic investing. It is a reminder that successful investing is fundamentally a long-term exercise in discipline. Markets will fluctuate. Headlines will change. Economic uncertainties will emerge and disappear. Through all of this, the greatest determinant of investment success is often not the market itself but the investor’s response to it. Most investors do not fail because markets disappoint them. They fail because emotions persuade them to abandon sound strategies before those strategies have had sufficient time to work. The evidence is increasingly clear. Markets reward discipline more consistently than they reward prediction. And perhaps that is the most important lesson every investor should remember.