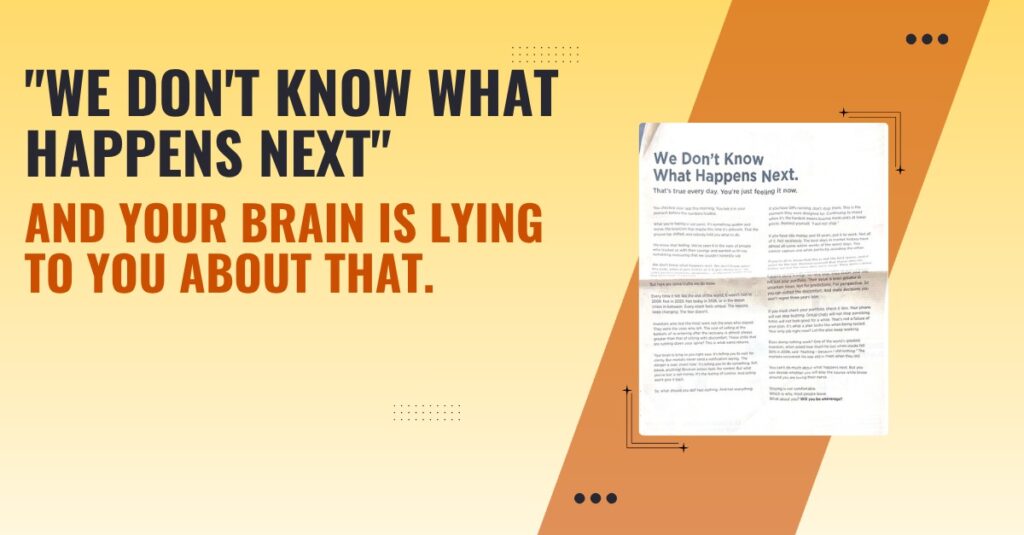

By now, you have likely seen it. A full-page advertisement in The Economic Times, dated April 4, 2026, published under DSP Mutual Fund’s investor education initiative. Its headline — “We Don’t Know What Happens Next” — stopped readers mid-scroll, mid-sip, mid-panic. Fund managers shared it. Analysts quoted it. WhatsApp groups forwarded it at 7 AM.

The reason it went viral is not because it said something new. It is because it named something investors were already feeling but could not articulate. That gap — between what we feel and what we understand about why we feel it — is precisely where behavioral finance lives.

This piece reads the advertisement sentence by sentence through the lens of behavioral science, names the specific biases and heuristics it addresses, and connects them to empirical research on investor psychology — including studies conducted during geopolitically turbulent periods strikingly similar to today’s.

The ad is not just good communication. It is an almost clinically precise map of how retail investors mentally collapse during market stress — and a gentle, evidence-based prescription for each failure mode.

The Heuristics and Biases at Work

The advertisement opens with a scene: you check your app and feel it in your stomach before the numbers load. This is not poetry — it is a description of somatic anticipatory anxiety, the physiological marker Antonio Damasio identified as central to financial decision-making. Before the rational mind processes data, the body has already voted.

The ad then names the real feeling: not fear broadly, but ‘the suspicion that maybe this time it’s different.’ This distinction matters enormously, and the behavioral literature is precise about why.

RESEARCH CONTEXT — AVAILABILITY HEURISTIC & RECENCY BIAS After a sharp market fall, investors do not think about the 90%+ of days when markets recovered. They think about the days they lost money — because those memories are more emotionally vivid and therefore more cognitively available. Nofsinger and Varma (2014) studied mutual fund flows during the 2008 crisis and documented that retail investors dramatically overweighted recent negative returns, pulling money at precisely the worst moments. Nofsinger & Varma (2014), Journal of Banking & Finance; Barber & Odean (2008), Review of Financial Studies |

The ad’s most behaviorally sophisticated line is this: ‘What you’ve lost is not money. It’s the feeling of control. And selling won’t give it back.’ Investors in downturns are not merely responding to numerical losses — they are responding to a loss of perceived agency. Selling at a devastating realized loss provides momentary psychological relief because it restores the illusion of control. This is Loss Aversion and the disposition effect operating simultaneously.

RESEARCH CONTEXT — LOSS AVERSION & THE DISPOSITION EFFECT Kahneman and Tversky’s Prospect Theory (1979) showed losses are felt ~2.5x as intensely as equivalent gains. Barberis and Xiong (2009) showed that realization utility — the pleasure of ‘closing the books’ on a position — is a powerful driver of selling during crashes. Investors sell not because fundamentals demand it, but because the act of selling provides emotional resolution. Kahneman & Tversky (1979), Econometrica; Barberis & Xiong (2009), NBER Working Paper |

The action bias — ‘Your brain is lying to you. It’s telling you to do something. Sell, pause, anything!’ — is another precisely named phenomenon. Under uncertainty and threat, humans have an evolved predisposition toward action over inaction, even when evidence suggests inaction is optimal. Odean (1999) showed the more frequently retail investors traded, the worse their net returns — yet trading continued, driven by the psychological reward of activity itself.

RESEARCH CONTEXT — GEOPOLITICAL RISK & INVESTOR BEHAVIOR Bali, Brown, and Tang (2017) found elevated geopolitical risk caused retail investors to significantly increase cash allocations and reduce equity exposure — but this shift was systematically mistimed. High geopolitical risk periods were followed by above-average equity returns in the subsequent 12 months in the majority of historical cases. Pástor and Veronesi (2013) showed political uncertainty depresses equity prices through discount rate spikes, not fundamental changes — temporarily pricing assets below their fundamental value. Bali, Brown & Tang (2017), Management Science; Pástor & Veronesi (2013), Journal of Financial Economics |

The Bias Grid — At a Glance

HEURISTIC Availability Heuristic Crash memories are vivid and accessible, making further crashes feel more probable than base rates justify. The ad counter-programs this with historical enumeration: 2008, 2020, 2026. | PROSPECT THEORY Loss Aversion Pain of loss outweighs equivalent gain ~2x. Selling provides momentary relief from loss-aversion pain. The ad reframes what is being lost — not money, but the illusion of control. |

COGNITIVE BIAS This-Time-Is-Different Fallacy Investors reject prior recovery precedents because the current crisis feels uniquely severe. The ad’s historical litany directly confronts this representativeness failure. | ACTION TENDENCY Action Bias Under threat, doing anything feels better than doing nothing. The ad reframes inaction as ‘letting the plan keep working’ — an active cognitive reframe. |

SOCIAL COGNITION Herding & Social Proof Observing peers exit signals private information, triggering cascades. The ad names this explicitly: ‘while those around you are losing their nerve.’ | EMOTIONAL SYSTEM Somatic Marking The body votes before the mind processes. ‘You felt it in your stomach before the numbers loaded’ names this pre-cognitive signal — and asks you to notice it rather than act on it. |

The Advertisement's Most Sophisticated Move

What commentators have largely missed: the ad’s most behaviorally sophisticated move is not the reassurance. It is the refusal to reassure.

The headline — ‘We Don’t Know What Happens Next’ — deliberately violates what investors usually seek from financial institutions: certainty. Every other actor in the ecosystem is busy predicting, forecasting, projecting. DSP chose to say: we do not know. Paradoxically, this admission of ignorance is more reassuring than any forecast — because it is true.

The advertisement is not telling you the market will recover. It is telling you that no one knows — and that the investors who have historically done best are the ones who stayed anyway.

The SIP line is equally sophisticated: ‘This is the moment they were designed for.’ This repositions the investor not as a victim of the crash but as someone executing a strategy built for exactly this scenario. Thaler and Benartzi (2004) showed that commitment devices — automating investment decisions — systematically protect investors from action bias during downturns, making good behavior the path of least resistance.

Conclusion

The biases the ad addresses — availability, loss aversion, herding, the this-time-is-different fallacy, somatic anxiety, action bias — are not flaws of weak investors. They are features of human cognition that evolved for environments very different from financial markets. Our brains, wired for immediate physical threat response, are meeting a novel challenge: probabilistic uncertainty about future paper wealth.

The advertisement holds up a mirror. It says: this is what your brain is doing right now, and you should know about it before you act. That is the highest aspiration of behavioral finance — not to make investors smarter, but to make them more aware of the specific ways in which they are predictably, humanly, forgivably irrational — and to create enough of a pause between feeling and action that they choose deliberately rather than reactively.

The views expressed are academic and educational in nature. This is not investment advice. Please consult a SEBI-registered financial advisor before making investment decisions.